403(b) vs. 401(k): Understanding the Differences and Similarities

Choosing the right savings method can make a huge difference in preparing you for the retirement you desire. Two of the most common employer-sponsored retirement plans are 403(b) and 401(k) accounts. In this guide, we’ll explore 403(b) vs. 401(k) plans, their similarities and differences, and how to determine which one is right for you.

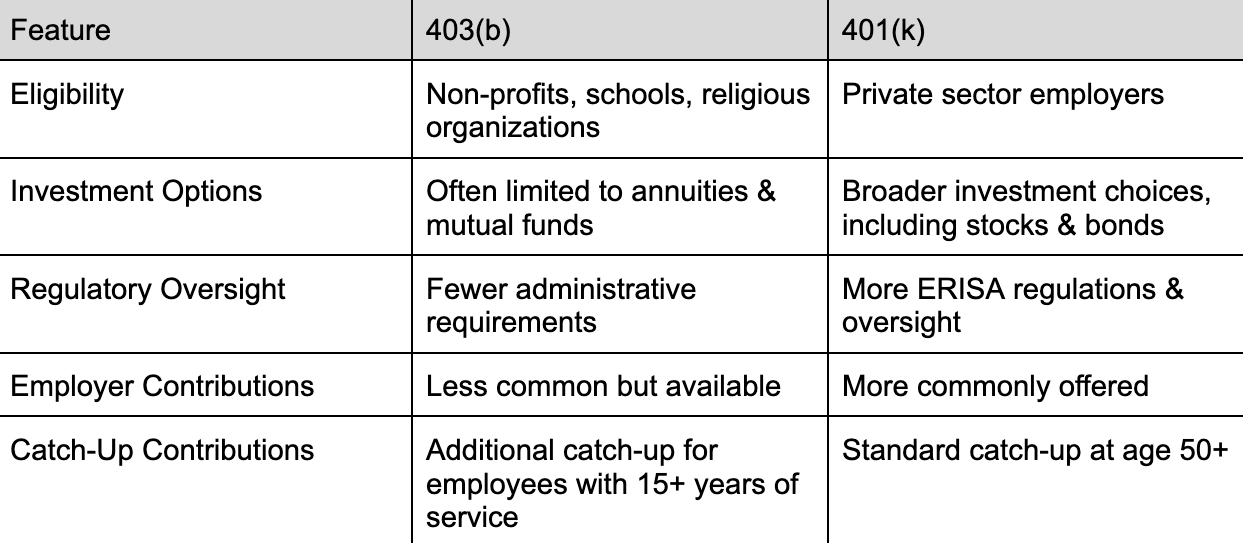

403(b) vs. 401(k) Plans

Both 403(b) and 401(k) plans are tax-advantaged retirement accounts offered by employers, allowing employees to contribute a portion of their salary to save for retirement.

401(k) Plan

A 401(k) plan enables employees in the private sector to contribute a portion of their salary on a pre-tax basis to a retirement account through automatic payroll deductions. Employees may only contribute up to an annual maximum dollar amount.

Investments within a 401(k) typically include mutual funds, stocks, and bonds, and funds grow tax-deferred until withdrawal. While withdrawals before age 59½ may incur penalties, 401(k) plans provide a structured and efficient way to build long-term retirement security.

An employer offering a 401(k) plan may also make matching contributions, up to a limit, and could also add a profit-sharing feature to the plan.

403(b) Plan

403(b) plans are typically offered by non-profit organizations, public schools, and certain tax-exempt employers. Similar to a 401(k), investments grow tax-deferred until funds are withdrawn, typically after age 59½ to avoid penalties.

While 403(b) plans offer the same basic retirement savings options, there are some distinctions:

- Vesting: A vesting schedule requires employees to fulfill a specified term of employment before accessing benefits. Some 403(b) plans offer quicker vesting periods than 401(k)s, or they might allow immediate vesting of employer contributions.

- Investment Options: Until 1974, 403(b) plans were limited to tax-sheltered annuities, but mutual funds are now allowed.

Many 403(b) plans offer mutual funds and annuities as investment options, and some employers provide matching contributions. With lower administrative costs and early withdrawal exceptions for specific circumstances, a 403(b) can be a valuable retirement tool for eligible employees.

Similarities Between 403(b) and 401(k) Plans

Despite serving different groups, 403(b) and 401(k) plans share several common features:

- Tax Advantages: Both plans allow for pre-tax contributions that can reduce taxable income, or Roth contributions that offer tax-free withdrawals in retirement.

- Contribution Limits: For 2024, employees can contribute up to $23,500, with an additional $7,500 catch-up contribution for those aged 50 and older.

- Early Withdrawal Penalties: Any distributions taken before age 59 ½ that don’t qualify for any exceptions will be subject to a 10% tax penalty, in addition to the ordinary income taxes you’ll pay on non-Roth retirement withdrawals.

- Employer Matching: Many employers offer matching contributions, though the percentages and structures vary.

- Investment Options: Both plans provide access to mutual funds and other investment vehicles to help grow retirement savings.

- Required Minimum Distributions (RMDs): Retirement account owners must take their first RMD for the year they become 72. The withdrawal amount is based on the account balance at the end of the previous year, along with the average life expectancy for a person of their age.

Key Differences: 403(b) vs. 401(k)

While they share similarities, there are distinct differences between 403(b) vs. 401(k) plans that can impact retirement savings strategies.

Which Plan Is Right for You?

Most employees won’t have a choice between a 403(b) vs. 401(k) plan, because the type of plan offered is determined by the type of employer. However, if a worker has multiple employers and access to multiple retirement plans, or if they are trying to choose between jobs with different plans, here are some things to consider.

- Investment Options: 403(b) plans have relatively limited investment options. A 401(k) plan will have more robust offerings.

- Employer Matching: Not every retirement plan offers employer matching. If you’re choosing between plans and one has an employer match, go with that plan. An employer match is a part of your total compensation package and equates to a 100% return on your investment.

- Roth Availability: Check whether your 403(b) vs. 401(k) plan offers a Roth option, so you can get tax-free withdrawals. Not all plans have this option.

Regardless of which plan you have, taking full advantage of employer matching, maximizing contributions and diversifying investments can significantly impact your long-term financial success.

Need Help Navigating Your Retirement Plan?

Choosing between 403(b) vs. 401(k) can be complex, but we’re here to help. We’re here to guide you through your options and help develop a personalized retirement strategy that aligns with your goals. Contact our team today.