Planning your exit from a family business is a transition that affects your family, your employees, and the legacy you have built over time. A thoughtful approach to family business and succession planning helps bring clarity to that transition and aligns your goals with a practical path forward.

This guide walks through when to start planning, how to define your goals, the most common exit strategies, and the key financial and relational factors that shape a successful outcome.

Key Takeaways

Before diving into the details, it helps to understand the big picture. A strong succession plan develops over time with clear intention and coordination across financial, legal, and family considerations.

- Start early to allow flexibility in tax strategy, valuation, and leadership transition

- Define clear goals around control, income, and legacy before choosing a structure

- Evaluate multiple exit paths, including family transfer, employee buyout, or sale

- Align valuation, liquidity, and estate planning into one cohesive strategy

- Address communication, roles, and governance alongside financial decisions

When these elements work together, the transition becomes more predictable and easier for everyone involved.

When Should You Start Family Business and Succession Planning?

The ideal time to begin is typically five to ten years before you plan to step away. Starting early gives you time to test different approaches, prepare successors, and adjust as your goals or market conditions change. Waiting too long often compresses important decisions into a narrow window, limiting options and creating unnecessary stress.

Signs It May Be Time to Start Planning

- You expect to step back within the next five years

- Your business has no clear successor in place

- You are unsure how to balance income needs with legacy goals

- You anticipate tax or regulatory changes

Early planning also makes it easier to complete foundational steps like updating agreements, obtaining a valuation, and preparing for potential tax implications.

What Does a Successful Transition Look Like?

A succession plan starts with defining what success means to you. This includes both financial and personal priorities. Without clarity around what you want, even well-designed strategies can fall short of expectations.

Key Decisions to Document

- Your role after the transition, whether fully retired or still involved

- How ownership and voting control will be structured

- Your income needs and any charitable intentions

- How to treat family members fairly, especially those inside versus outside the business

Putting these decisions in writing helps reduce future conflict and ensures your planning strategy reflects your true priorities.

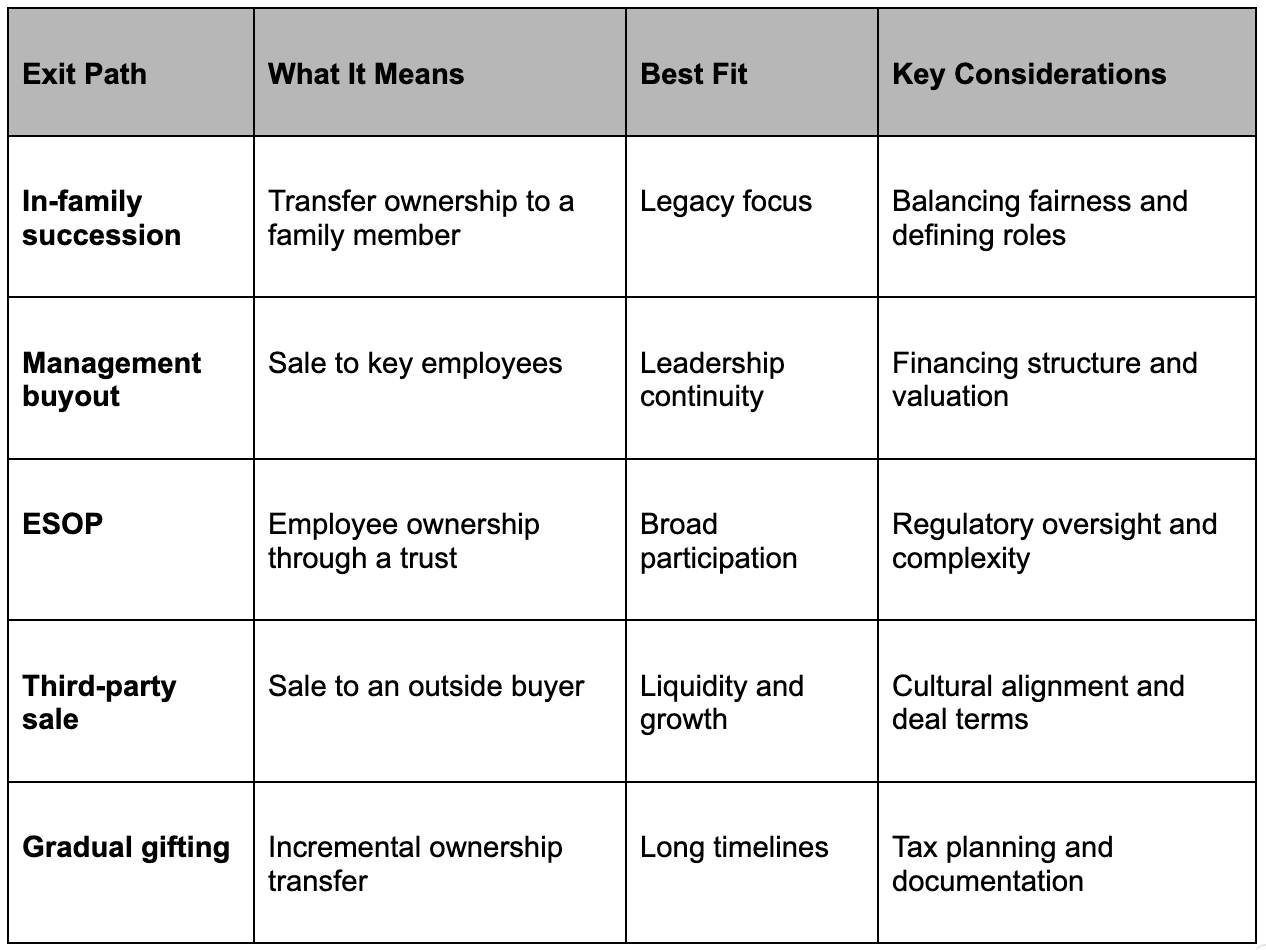

Comparing Your Exit Options

There is no single path that works for every business owner. Each option comes with tradeoffs in control, liquidity, and continuity.

Each approach should be evaluated within the broader context of your financial plan and long-term objectives.

How Valuation and Liquidity Influence the Plan

Behind every transition is a set of technical decisions that shape the outcome. A well-structured plan connects valuation, tax strategy, and funding sources so that ownership changes can happen smoothly.

Areas to Review

- Business valuation: A credible, independent valuation establishes fairness and supports tax compliance

- Buy-sell agreements: Define triggers, pricing methods, and funding mechanisms

- Liquidity planning: Identify how taxes, buyouts, and retirement income will be funded

- Estate coordination: Ensure your estate plan reflects your business intentions

These elements are often interconnected. Addressing them together creates a more durable and flexible plan.

The Human Side of Succession Planning

Family business transitions often succeed or fail based on relationships. Clear communication and defined roles can prevent misunderstandings and help maintain trust throughout the process.

Governance Practices That Help

- Hold regular meetings with clear agendas and documentation

- Define responsibilities and compensation for all involved

- Establish decision-making frameworks and voting thresholds

- Create a structured approach to conflict resolution

Pairing authority with mentorship is equally important. Gradually transferring knowledge and relationships helps successors step into leadership with confidence.

A Practical Timeline for Transition Planning

Most succession plans unfold over 18 to 36 months, though preparation often begins earlier.

Months 1–6

- Assemble your planning team

- Define goals and update communication plans

- Complete a business valuation

Months 7–12

- Begin transitioning responsibilities

- Model financial scenarios and funding strategies

- Align estate and ownership structures

Months 13–24

- Execute transfers and finalize agreements

- Test governance structures in practice

- Complete legal and tax reviews

Ongoing

- Review and adjust the plan every one to three years

A structured timeline helps maintain momentum while allowing flexibility as conditions change.

Frequently Asked Questions About Family Business and Succession Planning

When should I begin succession planning?

Most business owners start five to ten years before retirement to allow time to fully develop a strategy, training schedule, and tax plan.

What if no family member wants the business?

You can explore alternatives like selling to employees or a third party while still preserving the value you have built.

How is business value determined?

An independent business valuation provides a fair and defensible estimate for transfer or sale purposes.

Can multiple heirs share ownership?

Yes, but clear governance, voting rights, and communication structures are essential to help avoid conflict.

How often should I update my plan?

You should update your succession plan every one to three years, or after major life or business changes.

What role does insurance play?

Insurance can provide liquidity for buy-sell agreements or estate taxes, helping reduce financial strain during the transition.

Building a Transition Plan That Reflects What Matters

A successful exit is not just about transferring ownership. It is about carrying forward the relationships and values that shaped your business. With the right preparation, you can align financial outcomes with the future you envision for your family and your business.

Working with a financial professional can help bring all the moving pieces together, from valuation and tax considerations to communication and long-term planning.

If you are beginning to think about your transition, now is the time to put a plan in place. Connect with the Totus Wealth Management team to discuss your goals, explore your options, and build a strategy designed around what matters most to you and your family.