Required minimum distributions (RMDs) can feel like a tax clock you cannot pause. Even when you do not need the cash, the IRS still expects a distribution, and that can force trades or timing decisions you would not otherwise make.

With a market-aware approach, you can satisfy the rules while staying intentional about risk, taxes, and allocation. A solid RMD strategy comes down to three choices: what you distribute, how taxes get paid, and how you keep the portfolio aligned afterward.

Key Takeaways

Here is a quick summary of what this guide covers.

- In-kind distributions can satisfy the RMD without forcing a sale, which can help when markets are down or gains are concentrated.

- Withholding is optional at the account level, so you can satisfy taxes by increasing withholding through an IRA RMD to simplify estimated payments.

- Pairing the RMD with a rebalance can turn the requirement into a practical maintenance step, trimming overweight positions and replenishing cash for near-term spending.

- Coordinating RMD timing with charitable giving or capital gains planning can help manage tax brackets and potential IRMAA (Income-Related Monthly Adjustment Amount) tiers.

Taken together, these choices can help you meet the requirement while staying consistent with your goals and risk tolerance.

Where The RMD Choice Gets Complicated

RMDs apply to most pre-tax retirement accounts, including traditional IRAs and many employer plans. Once they start, the decision becomes a coordination exercise across taxes, cash flow, and portfolio exposure.

When markets are strong, selling to raise cash can feel straightforward. When markets are weak, selling can feel like locking in losses or disrupting positions you still want to own.

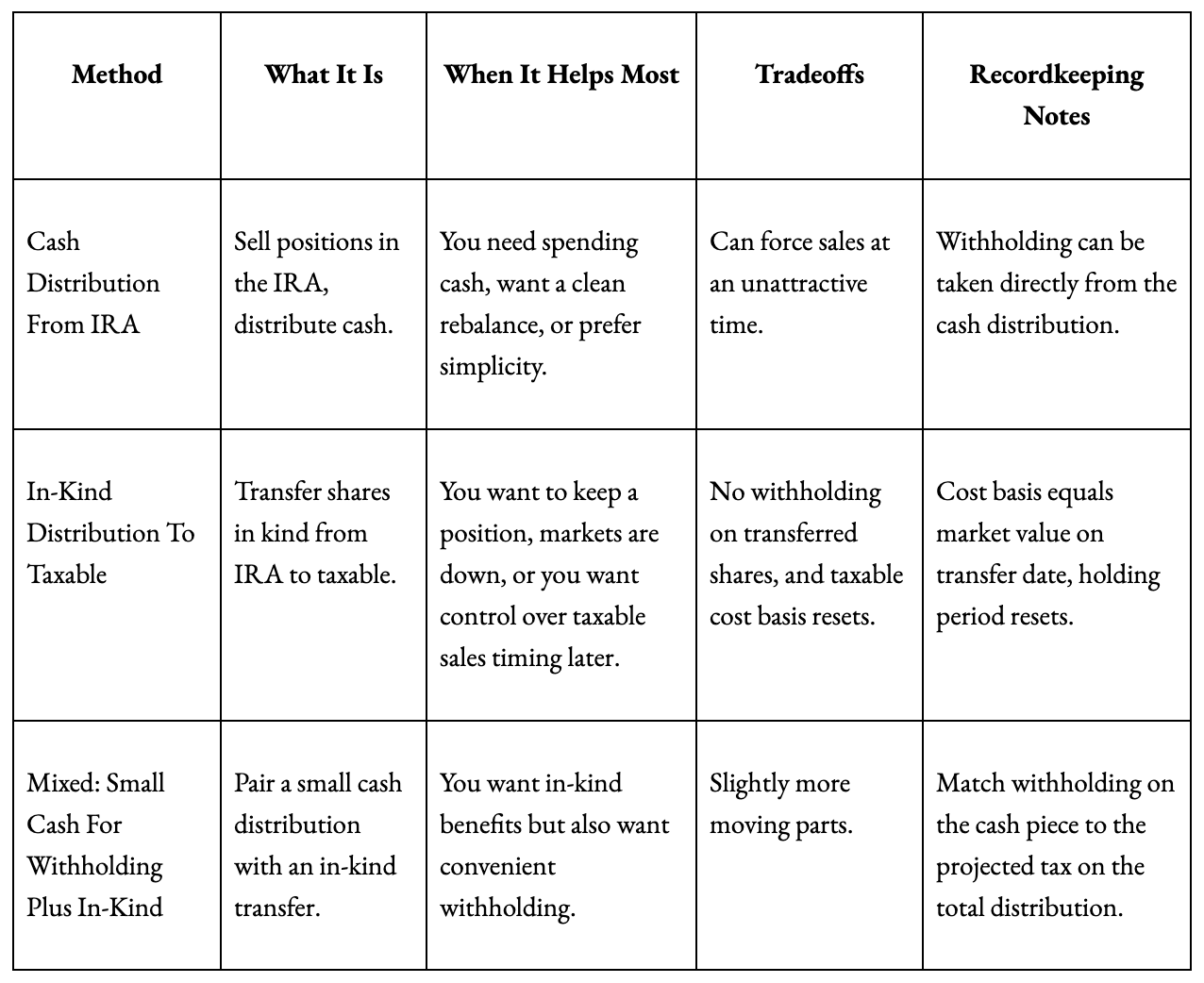

An RMD also does not have to be a cash sale followed by a distribution. You can move shares out of the IRA into a taxable account at the same market value, meeting the RMD without selling inside the retirement account.

You still owe ordinary income tax on the fair market value transferred on the distribution date. After the transfer, the taxable account establishes a new cost basis and holding period, and future gains or losses are typically capital in nature.

In-Kind Distributions: When Keeping The Position Can Be The Point

An in-kind distribution satisfies the RMD by transferring shares, not cash, from the retirement account to a taxable account. The value of what you transfer counts toward the RMD, based on the fair market value on the day of distribution.

This can fit when you want to keep a position intact, when markets are down, or when selling would force a portfolio change you did not intend. It can also fit when you want more control over the timing of taxable sales later, including sales that respect capital gain brackets and harvesting rules.

This approach is not automatically better. The fit depends on what your portfolio needs next: spending cash, a shift in allocation, or a clean way to meet the requirement without forcing trades.

Selecting Which Holdings To Move In Kind

Investors nearing retirement often hold a mix of equities, bonds, and cash across retirement and taxable accounts. If you transfer shares in kind, the selection matters because you are moving assets from one tax bucket to another.

A practical way to narrow the list is to ask three questions: does it make sense to hold in taxable given your goals, do you want to hold it through volatility, and does the move help manage drift versus your target allocation.

Some holdings may be more naturally taxable-friendly, such as positions you expect to hold long term, or holdings that support income goals in taxable. Regardless of what you choose, remember the tax mechanics: the distributed amount, cash or in kind, is ordinary income, and the taxable account’s cost basis and holding period reset on the transfer date.

Withholding: Turning The RMD Into A Tax Payment Lever

IRA distributions can include federal and state withholding. Many retirees choose to withhold directly from an RMD instead of making separate estimated payments during the year.

This can be especially helpful later in the year when you have a clearer view of wages, Social Security, pensions, interest, dividends, and realized gains. Because withholding is generally treated as paid evenly throughout the year, it can reduce or eliminate quarterly estimated payments.

Two cautions matter: you cannot withhold from shares moved in kind, and employer plan RMDs generally cannot be combined with IRAs, so confirm the rules for each account.

Staying Aware Of IRMAA And Adjusted Gross Income

For many retirees, thresholds matter, not just tax brackets. Medicare premiums can change based on income, and IRMAA is a common pressure point.

Because RMDs increase taxable income, they can raise adjusted gross income (AGI) and potentially push you into a higher Medicare premium tier. If you are close to a threshold, coordination matters, especially when other income decisions are also in play, such as charitable giving, capital gains, or Roth conversion planning.

The goal is to be deliberate about how income items stack in the same year. A simple projection can show whether you are near a bracket or an IRMAA tier before you finalize timing and withholding.

Rebalancing Around The RMD: Keep The Plan Intact

Market movement can push portfolios off target. RMDs create a natural moment to rebalance, because you are already taking action inside the account.

If the portfolio is overweight equities after a strong run, selling equities in the IRA to fund a cash RMD can trim risk while meeting the requirement. In that case, the distribution and the rebalance can become one clean transaction.

If markets are down and selling equities feels like the wrong move, an in-kind transfer can satisfy the RMD while keeping exposure. You can then rebalance inside the IRA after the transfer or rebalance elsewhere, depending on where drift is showing up.

Sequence of returns is often a concern near retirement because poor early returns can have an outsized impact once withdrawals begin. Rebalancing does not remove market risk, but it can help align risk with each part of the portfolio’s role, especially alongside a clear near-term cash plan.

RMD Fulfillment Methods Compared

Many retirees shift among these methods over time as markets, cash needs, and tax situations change.

A Simple, Annual RMD Planning Checklist

A repeatable sequence can reduce surprises and keep RMDs connected to your broader plan.

- Confirm the year’s RMD amount across all applicable accounts, and whether you can aggregate IRA RMDs and which account will fund them.

- Review the portfolio’s current drift versus targets, and identify positions that are candidates for trimming or transferring in kind.

- Project total taxable income for the year, including the RMD, then set federal and state withholding targets to avoid penalties.

- Choose the fulfillment method, cash, in kind, or mixed, then execute the transaction with enough time for transfer and withholding.

- After distribution, rebalance the remaining IRA to target weights, and plan taxable activity with capital gains and harvesting rules in mind.

Choosing A Timing Window That Fits Your Plan

RMDs can be taken early, spread through the year, or completed near year-end. Each timing choice can work, as long as it aligns with your cash flow and tax planning style.

An early-year RMD can simplify the calendar and reduce the risk of missing the requirement. A spread-out approach can smooth cash flow and reduce the feeling of timing the market with one large trade. A year-end RMD can be useful when you want more information before you lock in decisions, especially if you are watching brackets, realized gains, or IRMAA thresholds.

The best timing is usually the one that matches how you actually manage income and taxes, and many retirees adjust timing year to year as conditions change.

Coordinating The RMD With Other Goals

RMDs do not exist in a vacuum. Charitable goals, Roth conversion planning, and capital gains decisions can all affect how the RMD lands on your tax return.

If charitable giving is part of your plan, it can be worth coordinating the timing and method of the RMD with those goals. If you expect significant capital gains, coordination can help you see the combined impact before income items stack too high in the same year.

Cash management matters as well. If spending needs are predictable, you may use the RMD to refill a cash reserve for near-term expenses so you are not forced to sell taxable assets later to raise money. The right approach can change across seasons of retirement and across different market environments.

Frequently Asked Questions About RMD Strategies

The questions below address common decision points as your RMD approach evolves.

Can I take one large RMD from a single IRA to cover all my IRAs?

Yes, IRA RMDs can be aggregated across traditional IRAs, then taken from one IRA. Employer plan RMDs are usually different and often must be taken separately from each plan, and they generally cannot be combined with an IRA, so confirm plan specifics before acting.

How do taxes work if I transfer shares in kind?

You owe ordinary income tax on the fair market value of the shares on the distribution date. In the taxable account, those shares receive a new cost basis equal to that value, and the holding period starts anew. Future gains or losses will be capital in nature.

What if I need withholding but prefer an in-kind distribution?

Use a mixed approach. Take a small cash distribution with sufficient withholding, then satisfy the remainder with an in-kind transfer. This combines administrative ease with portfolio flexibility.

Should I rebalance before or after the RMD?

Either works, as long as the end state matches your target allocation. Plan the sequence so you avoid accidental drift, and plan any taxable rebalancing with capital gains in mind.

Making RMDs Work With Your Portfolio

A market-aware RMD strategy can turn a rule into part of portfolio maintenance. When you coordinate what to distribute, how to handle withholding, and how to rebalance, you can meet the requirement while keeping the plan intact.

Details tend to matter most as you near retirement and in early retirement years, when cash flow, volatility, and Medicare premiums all matter. If you would like help modeling scenarios or aligning your RMDs with your overall allocation, connect with your financial professional to explore which levers fit best for your accounts and timeline.